The Cost of Mental Health Treatment

A Series About Navigating Mental Health

In this series, we will be looking closer at our mental health system and disparity of care. Last week we discussed the gap of treatment and asked the question: if I’m not “in crisis” but I’m not ok, where do I get help?

Readers, please note that I work hard to limit my newsletters to 6 minutes or less but this one is closer to 8 minutes! I simply couldn’t leave out more data analysis after writing about “Elsa.”

Be sure to follow along as we explore these topics in the coming months. You can also support me as a paid subscriber for $5 a month, which helps me keep up on my own treatments and time sneaking away to write in cafes.

I am not a medical professional and none of these writings should be considered as a professional or legal recommendation for treatment. Sites that are linked by Motherhood Minute are not monitored or investigated. Please refer to them at your own risk and awareness.

In full disclosure, my interest in mental health treatment derives out of my own experiences over the past 15 or so years. I have tried in-person counseling, teleHealth, medication treatment, and self-help resources. The questions are often the same:

Why is this costing me so much time and energy? What can I buy to feel better? How do I afford health insurance? Can I afford counseling? Do I have the money to spend on more help or should I wait?

Some numbers to consider…

“The recent KFF Survey of Consumer Experiences with Health Insurance found 17% of insured adults indicated that even with health coverage, they did not get mental health care that they thought they needed in the past year. Of these individuals, more than 4 in 10 (44%) indicated that one of the reasons they did not get needed mental health care was that they could not afford the cost.”1

According to Mental Health America:2

Almost a third (28.2%) of all adults with a mental illness reported that they were not able to receive the treatment they needed.

42% of adults with AMI (a mental illness) reported they were unable to receive necessary care because they could not afford it.

Nationally, 1 in 10 youth who are covered under private insurance do not have coverage for mental or emotional difficulties – totaling over 1.2 million youth.

In the U.S., there are an estimated 350 individuals for every 1 mental health provider. However, these figures may actually be an overestimate of active mental health professionals, as it may include providers who are no longer practicing or accepting new patients.

According to Reuters: The Federal Reserve reported in 2023 that “Fifty-four percent of adults said that their budgets had been affected "a lot" by price increases, with parents of children under 18, Black and Latin American adults and those with disabilities ranking among the most likely to report an impact from inflation.” 3

Numbers show us a broad stroke of how individuals in the United States are currently being affected by inflation, politics, and the post Covid removal of payment delays and government assistance programs ending.

Numbers, however, don’t show the big and small sacrifices people must make, especially if they need mental health care.

Where we see the cost…

The amount of money that must be spent for those who struggle with mental health care is incalculable but we can try to identify where the gap exists between affordable and accessible resources.

Let’s look at how someone might incur costs in their journey for help (not including potential challenges for those in minority communities or with chronic illness). I’m going to use the fictional name Elsa here because my toddler has insisted we watch a certain animated character forever (and Elsa honestly could use some counseling too, right?)

Elsa finds herself overwhelmed by her inner monologue daily and wonders if she could get help, but she’s not sure what help looks like. She goes online to Google her symptoms, which identify it as likely anxiety or depression, and searches for counseling services.

She knows she has insurance, so she goes to her insurance website and finds a provider search, where she calls offices to see if they are available. This takes multiple sittings over a week and leaves her feeling hopeless and exhausted; everyone replies they have no availability or are booked for two months. She finally makes an appointment with someone 30 minutes away and makes a note to ask her manager for the 2.5 hours of unpaid time off work when her visit happens two months later.

Elsa goes about her days and then comes across a triggering event followed by an argument with her sister, which leaves her feeling more on edge than usual. She calls the therapist office to see if they can meet sooner but they cannot.

Elsa goes back online and decides to search for an anxiety support group. There is a monthly meeting that meets every fifth of the month but she’s missed it. She has no outside support group she can turn to (you know because of those childhood trust issues and isolating times.)

She starts finding generic information suggesting to eat healthier, take supplements, exercise, and meditate.

Elsa lives in a rural and cold area where the weather makes it difficult to exercise outdoors. She buys Vitamin D supplements for $25 and a gym membership that costs her $60 a month. Her counseling office calls back and say her insurance has approved her for $30 copay per visit but she must pay $150 for the intake appointment.

When she finally sees her therapist, she has had to cancel her gym membership to afford the hour session. Her therapist gives her some evaluations and decides she needs to start with weekly counseling sessions. She can visit them after work in the future but she will have to negotiate with her manager to leave slightly earlier to make the appointments in time, which is more lost pay.

As her treatment expenses come in, her anxiety increases. When she leaves a voicemail for her primary care provider, they call back and suggest trying a low dose medication. Agreeing, Elsa goes to the pharmacy and pays $15 for the monthly prescription copay.

After a month visiting her therapist, Elsa is still feeling uncomfortable and distressed. Her friend recommends a trauma counselor who has a private practice that is out of network. She can submit for potential reimbursement but she will have to pay out of pocket for each session $150.

Elsa leaves her first therapist and gets in quicker with her new counselor. Thankfully they work well together but Elsa worries about her ability to pay. She relies more on her credit card for payments and buys cheaper groceries over produce to help with her cost of living. The reliance on filling and cheap foods like oatmeal, potatoes, and pasta causes her weight gain and she feels depressed.

Six months later she finds herself less anxious and has more techniques to cope with her childhood past, but she knows there is much more work to be done. She finds herself deciding if she can afford her current place of rent or if she should move in with family. She wonders if she is stable enough to get off medication. She considers getting an evening or weekend job to avoid any moves altogether…

Elsa’s imaginary rollercoaster of seeking care is compiled from a long list of messages I have received along with my personal journey for treatment. Let’s continue to examine the numbers behind the emotional journey.

A confusing landscape of care

If we look at the data from surveys done by KFF and Mental Health America alone, we can begin to see that polled Americans were most likely to cite reasons for not seeking mental health care due to the complicated terms and unaffordable costs of their healthcare plans. It should be noted that these surveys also show more negative claims of insurance benefits by individuals experiencing poorer physical or mental health.

If you consider the well-documented symptom of “inability to focus” that comes with mental health conditions, is it a wonder that insurance policies are often too difficult to understand for those experiencing depression, anxiety, or chronic pain?

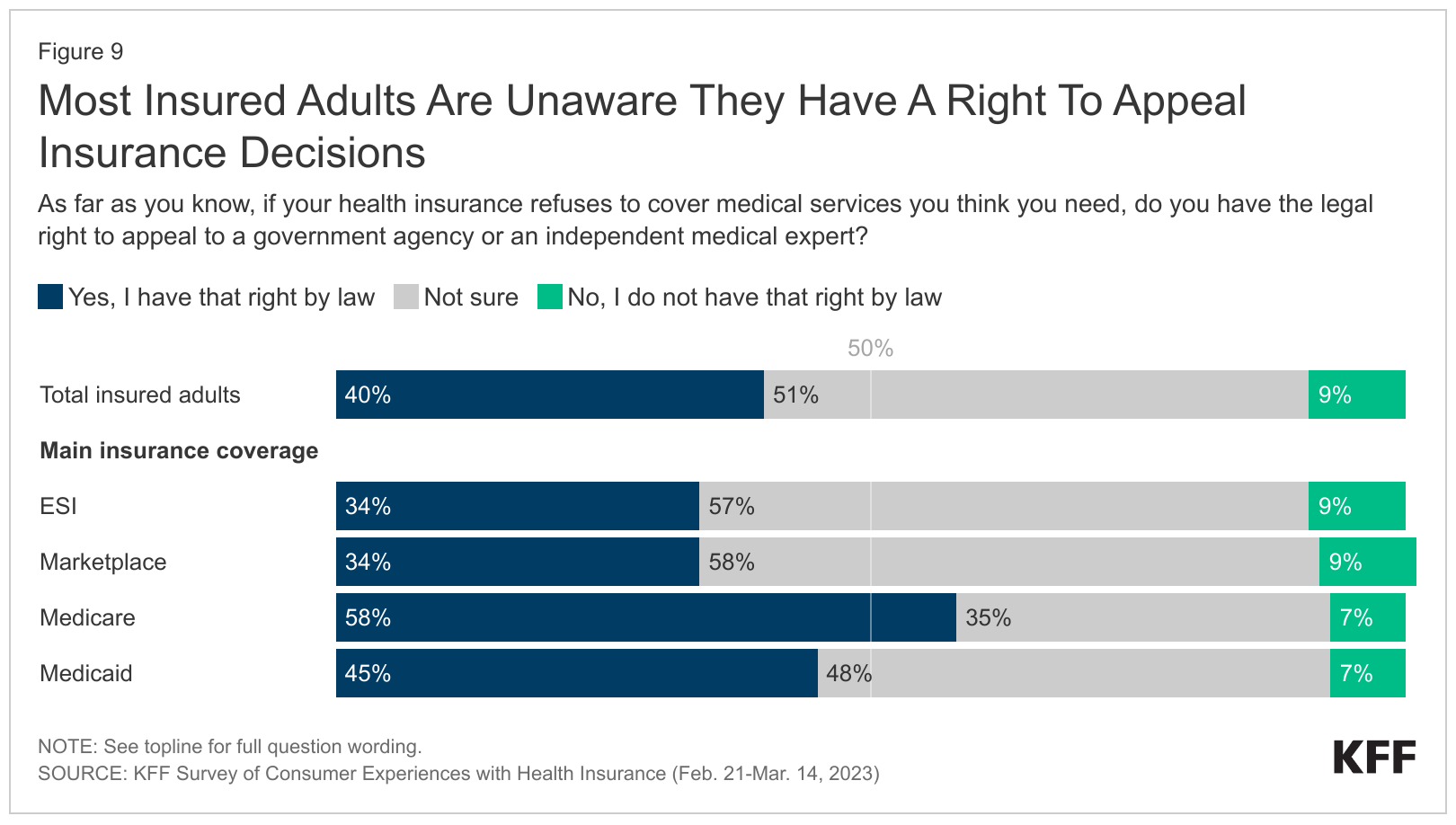

For example, most insured adults are unaware they have the right to appeal insurance decisions. KFF writes, “Four in ten insured adults (40%) know they have a legal right to appeal to a government agency or an independent medical expert if their health insurance refuses to cover medical services they think they need.”4 We have to ask if this comes from a complex healthcare system or a lack of energy to be one’s advocate.

This inaccessibility to care can also include a lack of language translations/translators for non-English speaking communities, a lack of healthcare providers that can help these communities with greater cultural understanding, and the stigma many cultures give to mental health conditions or treatment.

Where do we go from here?

Our next step will be to suggest practical ways mental health advocates and organizations can adapt their information sharing to be reader-focused instead of provider-focused.

We will move forward with more personal stories about the mental health gap, look at how self-care products are being advertised to those who cannot afford them, and more. If you are interested in writing a 950-1200 word article as a guest writer, you can submit that inquiry to hello@chanelriggle.com

What are your own experiences with seeking mental health care? Where is the gap? What challenges have you faced you’d like to see in this series?

https://www.kff.org/mental-health/issue-brief/proposed-mental-health-parity-rule-signals-new-focus-on-outcome-data-as-tool-to-assess-compliance/

https://mhanational.org/issues/state-mental-health-america

https://www.reuters.com/markets/us/inflation-has-eroded-us-households-financial-security-fed-survey-shows-2023-05-22/

https://www.kff.org/private-insurance/poll-finding/kff-survey-of-consumer-experiences-with-health-insurance/